Check Your FREE Credit Score in 30 Seconds

Instant, secure & always free

Powered by

Soft enquiry only | No impact on your Credit Score

100% secure. Takes less than 1 minute.

Free Credit Score & Experian Credit Report - How to Boost Your Credit Score

What is Credit Score?

Credit score is a 3-digit number displayed on your credit report. It provides a snapshot of your credit history to lenders which helps them make decisions about your eligibility for loans and credit cards. Checking your credit score helps you correct any errors and maintain or build a good credit score, which has numerous benefits for you. Check your credit score for free right here!

Your credit report is a summary of your entire credit history, from loans to credit cards, both active and closed. This is based on data collected from lenders and collated by the four major credit bureaus in India. It gives lenders crucial information about your creditworthiness.

How to Check Free Credit Score on BankBazaar

Steps To Get Your Free Experian Credit Score on BankBazaar:

- Visit the BankBazaar credit score page.

- Enter your first and last name.

- Add your mobile number and e-mail ID.

- An OTP will be sent to your mobile number for verification.

- The next step would be to verify your age.

- Your free credit score will be displayed on the screen.

You can also check your credit score for free on the BankBazaar mobile app. Download the app on Google Play or the App Store and follow the steps given above to get your free credit score.

Why Check Your Credit Score?

Checking your credit score and monitoring your credit report can help you build and maintain an excellent score. By tracking your progress consistently, you can make sure that your repayments are recorded correctly, identify any errors or false information immediately, and resolve such errors quickly by reporting them to the relevant credit bureau. This helps to avoid any negative impact on your credit score.

Why Track Your Credit Score Regularly?

🔒 100% secure. Takes less than 1 minute.

How Frequently Should You Check Your Credit Score?

It is a good habit to check your credit score on a quarterly basis or a minimum of once a year. Tracking your credit score a few months before applying for a big-ticket loan is also a good idea as it helps you correct or maintain your credit score before you submit your loan application. You should also check your credit score after you have closed a loan account or credit card in order to make sure that the closure is reflected in your credit report.

What is a Good Credit Score in India?

In India, a credit score above 700 is considered as good by credit bureaus; 750 and above is considered as excellent.

How Are Good Credit Scores Helpful?

A good credit score gives you an advantage when applying for loans or credit cards. The higher your credit score, the more likely it is for lenders to offer you loans at attractive interest rates. It also makes the process of credit card or loan applications smoother and faster.

What are the Benefits of a Good Credit Score?

Here are the benefits of a good credit score.

- Get The Best Credit Card - A good Credit Score may get you the best Credit Cards. Get a feature-loaded card and reap the benefits.

- Quick Loan Approval - A good Credit Score works like an expressway for your loan application. Banks may approve your application quickly and readily.

- Better Interest Rate - With the backing of a good Credit Score, you can bargain for a lower rate of interest on loans and Credit Cards.

- Loans Made More Affordable - Loans come saddled with processing fees and many other charges. You can bargain your way out of some of these charges with a good Credit Score.

- Visa Applications - A good score may help in getting your visa application approved as many countries consider the credit history of the applicant in their approval process.

Get your free Credit Score right away and see if you are eligible for all these benefits. You can check your score on BankBazaar at zero cost.

Key Factors Impacting Your Credit Score

Payment History

On-time EMI & card bill payments

35%

Credit Utilization

Percentage of available credit used

30%

Age of Credit

Average age of all open credit accounts

15%

Total Accounts

Total open/closed credit accounts

10%

Credit Enquiries

Total hard enquiries by lenders

10%

Negative Accounts

Written-off or settled accounts

🔒 100% secure. Takes less than 1 minute.

Credit Bureaus in India

The four major credit bureaus in India that are licensed by the Reserve Bank of India are Experian, TransUnion CIBIL, CRIF High Mark, and Equifax. These are also called Credit Information Companies (CIC).

Experian Credit Score Range in India

Experian credit scores in India range between 300 and 850. The different Experian score ranges are mentioned in the table below:

Experian Score Range | Meaning |

NA/NH | Indicates no credit history. |

350 - 549 | Poor - very low chances of loan/credit card approvals |

550 - 649 | Fair - Loan/credit approvals possible but with higher interest rates |

650 - 749 | Good - indicates a low-risk borrower |

750 - 799 | Very good - increased chances of loan/credit card approvals |

800 - 850 | Excellent - higher chance of approvals, lower interest rates, and added benefits |

POOR

300 – 549

Experian Credit Score Range and What It Means

●

Low chance of credit approval. Needs serious work.

🔒 100% secure. Takes less than 1 minute.

CIBIL Score Range in India

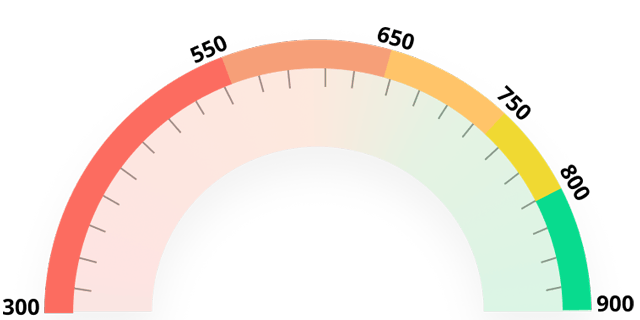

CIBIL scores in India range from 300 to 900 and have differing impacts on loan applications, as given below:

CIBIL Score Range | Meaning |

750 - 900 | Excellent - easier to get loan approvals at competitive interest rates |

700 - 750 | Good - loan approvals at standard interest rates |

550 - 700 | Average - eligible for loans but with a high collateral or higher interest rates |

300 - 550 | Poor - lower chances of loan approval |

Free Credit Report vs Paid Experian Credit Report - The Difference

The main difference between free and paid credit reports is the depth of information available in each.

Free credit reports will typically give you the latest credit score as well as a summary of your credit accounts and enquiries that were made by lenders (in case of loan or credit card applications).

Paid Experian credit reports will provide your latest credit score and a detailed record of all your credit accounts (both closed and active loans or credit cards), details of the credit account (lender's name, account number, date opened or closed, amount borrowed, amount outstanding, etc). It also provides the full list of enquiries made on your credit account. You also get a comprehensive credit summary.

Quick Guide to Improve Your Credit Score

Listed below are effective ways to improve your credit score:

- Pay your credit card bills and EMIs on time

- Avoid paying credit card bills partially; pay the full amount.

- Try to keep your credit utilisation ratio below 30% of the available credit.

- Do not close old credit cards, as their account history can help you boost your credit score.

- Try to maintain a healthy mix of credit products and ensure their dues are paid on time.

- Avoid applying for multiple loans or credit cards within a short span of time. This can lead to hard enquiries, which may impact your credit score.

- Check your credit report regularly for any errors; if errors are found, report them to the credit bureau immediately.

How to Improve Your Credit Score

Pay on Time

Timely EMI/card payments build credibility

Control Credit Utilisation

Keep usage below 30% of your limit

Review Reports for Errors Regularly

Check & dispute any errors immediately

Space Out New Credit Applications

Don't submit credit applications frequently

Maintain A Healthy Mix

Diversify with a mix of secured & unsecured credit

🔒 100% secure. Takes less than 1 minute.

Factors that Lower Your Credit Score

Knowing the factors that can lower your credit score can help you to avoid them. It is understood that having a high outstanding balance on your credit card can significantly reduce your credit score. Apart from that, there are several other factors that can hurt your credit score:

- Being late on your credit payments.

- Completely ignoring your loan dues/credit card bills.

- Creditors charge off accounts when credit card bills are not paid on time, and this can harm your credit score.

- Lenders often use third-party debt collectors to retrieve the loan amount from you, in case they do not receive payments. Having your account sent to collections reflects very poorly on your credit score.

- Filing for bankruptcy can have a devastating effect on your credit score.

- Closing a credit card with an outstanding balance drops your limit to Rs.0, similar to maxing out your credit card.

- Closing old credit cards shortens your credit history.

- Avoid applying for multiple credit cards or loans within a short duration.

- Relying on one type of credit mix can harm your credit score. Try to balance it out.

Factors that Do Not Affect Your Credit Score

Listed below are some of the factors that do not have any impact on your credit score:

- Where you live, your past or present address does not have any impact on your credit score.

- Your age, caste, creed, or marital status does not have any effect on your credit score.

- Your current salary, employment status, employer, or even employment history does not have any impact on your credit score.

- Your educational background or academic qualifications do not have an impact on your credit score.

- Your debit card usage or debit card history does not influence your credit score.

- Checking your own credit report multiple times or frequently will not lower your credit score.

Why Lenders Check Credit Scores Before Approving Loans

Lenders will look into your credit score to see how credit worthy you are. The closer your credit score is to 900, the higher the chances that the lender will approve your loan application. This is because a high credit score reflects a credit history with timely payments and no defaults or delays in repayments, which shows the lender that you are capable of repaying the loan.

Credit Score for NRIs

NRIs do have a credit score in India based on their credit history (loans and credit cards). This can be obtained and tracked through the credit reports issued by the relevant credit bureaus in India.

Credit Report Errors - Dispute Resolution

If there are errors on your credit report, you can resolve them by raising a dispute to the relevant credit bureau.

Experian: If there's an issue with your Experian credit report, contact customer care on the phone number 022-6641-9000 or send an email to consumer.support@in.experian.com. Registered users can log into their account on the official Experian website to raise a dispute; select ''Dispute'' and then ''Raise a Dispute''; select the relevant dispute type and enter the required details; click on ''Submit''.

CIBIL: Registered users should log into their account on the official CIBIL website; click on ''Raise a Dispute'' and then ''Access Dispute Form''; fill up the required details in the applicable section and submit the form.

CRIF High Mark: Registered users should log into their account on the official CRIF Highmark website; click on ''My Report'' and then ''Raise a Query''; select the credit report which is disputed and click on ''Proceed''; select the account that is disputed; click on ''Proceed''.

Equifax: Registered users should log into their account on the official Equifax website; navigate to the ''Dispute Center'' and click on ''File a Dispute''; click on the information to be changed and upload the required documents; click on ''Submit''.

How is Credit Score Calculated?

Credit bureaus calculate the score based on parameters such as repayment history, credit card usage (credit utilization ratio), Total accounts (loan + credit cards), credit enquiries and age of credit.

What are the Types of Enquiries on Credit Reports?

When it comes to checking credit score, there are two types of enquires, hard and soft enquires. Hard enquiries may decrease you Credit score by few points, While soft enquiries do not impact your Credit score.

A hard enquiry is when a financial institution checks your Credit Score to take a decision on your credit application. Every time you apply for a loan or a Credit Card, the lending institution checks your score and it is regarded as a hard enquiry. One to two hard enquires in a year don not usually impact the score.

When you check your own credit score, it is called a soft enquiry, and it has no impact on your score.

TIP: If you are applying for a loan or a Credit Card, do not apply to many banks at the same time. Too many enquiries will hurt your Credit Score.

4 Credit Score Secrets

Credit Score is one of the most misunderstood topics in the financial book. Here are four secrets to help you understand your Credit Score better.

Credit Score and Credit Report

Your Credit Score is calculated based on information present in your credit report. Your credit report presents details about your credit accounts, credit application and debt repayment, among others.

Checking Your Score Will Not Hurt It

When you or a company enquires about your Credit Score, it's called a soft enquiry and it does not hurt your credit score.

Credit Score Math

There are five prime factors that go towards deciding your Credit Score. They are - debt repayment, credit utilisation ratio, average credit age, type of credit account (secured / unsecured) and Credit Score enquiries made.

Keep an Eye On Fraud

You did nothing wrong and yet your Credit Score is low? Please go through your Credit Report thoroughly and immediately report any unauthorised activities to your bank to correct your score.

Before you plan to get an application approved keep a track of your credit score on regular basis either by taking free CIBIL score or subscription based CIBIL score. Scores normally range from 300-850.

Difference between Credit Score, Credit Rating, Credit Report

Credit Report | Credit Score | Credit Rating |

Your credit report has information on the current and past credit agreements that you hold. These include mortgages, credit card accounts, student loans, and inquiries on your credit history. | A credit score is similar to a grade that is provided to your credit report. It is a 3-digit number that usually ranges from 300 to 900. | A credit rating functions as an indicator of an organisation's ability to repay its loans. |

The credit report reflects your credit management, and you have control over the listings there. | The credit reporting bureau assigns you the credit score based on your credit history. | In order to determine whether or not these borrowers will be able to repay loans on time, specialized credit rating agencies analyse their financial risk. |

In order to access your credit report, you can get in touch with credit reporting agencies or use a credit monitoring service that offers you this information. | Your credit score is a part of the exhaustive credit report that you receive from the credit bureau. | The highest credit rating is AAA or A1, which demonstrates safety in terms of principal and interest repayment. D is the lowest possible rating. |

Disclaimer

Display of any trademarks, tradenames, logos and other subject matters of intellectual property belong to their respective intellectual property owners. Display of such IP along with the related product information does not imply BankBazaar's partnership with the owner of the Intellectual Property or issuer/manufacturer of such products.

Know More About Experian

Experian was established in India in 2006. It was licensed by the Reserve Bank of India (RBI) as a credit bureau in 2010. It was the first credit bureau in India to be licensed under the Credit Information Companies (Regulation) Act (CICRA) of 2005. It is among the four major credit bureaus in India. Experian is a global information services company that provides data and analytical tools across 90 countries with the goal of improving financial health for all.

Know More About CIBIL

TransUnion CIBIL is one of the leading credit information companies in India. The company maintains one of the largest collections of consumer credit information in the world. CIBIL Score plays a key role in the lives of consumers. Banks and other lenders check the CIBIL Score of the applicants before approving their loan or credit card application. Consumers can visit the official website of CIBIL to check their CIBIL Score and Report.

FAQs About Credit Score & Credit Report in India

1.How can I improve my Credit Score?

There are several ways to improve your credit score such as paying your loan EMIs and credit card bills on time, keeping your credit utilisation ratio below 30% of your available limit, and avoiding applying for multiple loans or credit cards within a short period.

2.Who can access my credit report?

Your credit report can be accessed by you, lenders (such as banks and non-banking financial companies), and government-recognised regulatory bodies. Lenders access your report when you apply for a loan or credit card, which counts as a hard enquiry. When you check your own report, it is a soft enquiry and has no impact on your score.

3.What factors are used to calculate a credit score?

Some of the main factors that are used to calculate a credit score are credit enquires, total number of accounts, age of credit, credit utilization ratio, and payment history.

4.What kind of information is not included in a credit report?

A credit report does not contain information about your savings or current accounts, your criminal record, your medical history, your lifestyle choices, your caste, religion, or marital status, or your salary and employment history. Debit card usage is not recorded on a credit report as well.

5.How long does information stay on a credit report?

In India, most credit bureaus keep information on your credit report for a period of up to seven years from the date the account was last active or the date of default.

6.What should I do if I find errors in my credit report?

If you notice any incorrect or outdated entries on your credit report, you should raise a formal dispute with the credit bureau that issued the report.

7.Can I have more than one credit report?

Yes, in India, there are four licensed credit bureaus, and each one maintains its own credit report and calculates its own credit score for you.

8.Are there any charges to check your credit score?

Usually, no charges are levied to check the credit score.

9.What is the highest possible credit score?

Usually, the credit score ranges between 300 and 900. However, depending on the credit information company, the credit scores may vary.

10.Will owning multiple credit cards affect my credit score?

Owning multiple credit cards does not automatically hurt your credit score. However, if you use a huge proportion of your credit limit across all cards, your credit utilisation ratio will rise, and your score may fall.

11.What is considered a good credit score in India?

In India, a credit score above 700 is generally considered good by lenders. A score of 750 or above is considered excellent and gives you the best chance of loan or credit card approval at competitive interest rates.

12.What is an Experian credit score?

An Experian credit score is a 3-digit number that ranges from 300 to 900. It is calculated by Experian India based on your credit history, including your repayment track record, credit utilisation, age of credit accounts, and the number of credit enquiries.

13.What are the major credit bureaus in India?

There are four credit bureaus in India are Experian, TransUnion CIBIL, CRIF High Mark, and Equifax India.

14.Is a credit score same as the CIBIL score?

A CIBIL score is a type of credit score that is issued specifically by TransUnion CIBIL Limited, which is one of the four licensed credit bureaus in India.

15.Can I get a loan in India with a low credit score?

It is possible to get a loan in India even if your credit score is low as some lenders may still approve your application for smaller loan amount. However, the interest rate that will be levied may be high.

16.Will closing a credit card affect my credit score?

Yes, closing a credit card can affect your credit score in two ways. First, if you close an old card, your overall credit history will shorten, which may reduce your score. Second, closing a card reduces your total available credit limit, which means your credit utilisation ratio could rise, which may reduce the credit score.

17.How do I report a wrong entry on my credit report?

You can report a wrong entry on your credit report by raising a dispute directly with the credit bureau that produced the report.

18.What is the impact of multiple credit enquiries on your credit score?

Every time you apply for a loan or credit card, the lender makes a hard enquiry on your credit report, which can reduce your score by a few points. If you make several applications within a short period, multiple hard enquiries can signal financial distress to lenders and your credit score will fall.

19.Why was I denied a loan despite having a good credit score?

Being denied a loan despite having a good credit score can happen for several reasons. such as a high debt-to-income ratio, too many hard enquiries in a short period, or the lender's own internal lending policies.

20.What does ‘New to Credit’ mean?

New to Credit (NTC) refers to individuals who have no prior credit history such as never taken out a loan and have never held a credit card.

21.Does checking my own credit score reduce it?

No, checking your own credit score is a soft enquiry and has no impact on your credit score, regardless of the number of times you do it.

22.How long does it take to improve my credit score?

There is no fixed timeline for improving a credit score, as it depends on why your score is low in the first place.

23.What happens to my credit score if I miss an EMI payment?

Missing even a single EMI payment can have a negative impact on your credit score, particularly if the payment is overdue by 30 days or more.

24.Does my salary or income affect my credit score?

No, your income or salary does not directly affect your credit score. Credit bureaus do not have access to your salary data, and it is not a factor in credit score calculations.

25.What does a credit score of –1 or NH/NA mean?

A credit score of –1, or a status of No History (NH) or Not Applicable (NA), means that the credit bureau does not have enough information to generate a numerical score for you.

26.How does debt settlement affect my credit score?

Settling a debt, where the lender agrees to accept a lower amount than what is owed, is recorded on your credit report as a ‘Settled’ account, which is viewed negatively by future lenders. A settled account indicates that you did not repay the full amount borrowed, which can remain on your credit report for up to seven years and make lenders wary of approving future applications.

27.Is it safe to check my credit score online?

Yes, checking your credit score online through authorized platforms is safe.

CIBIL Score Requirements for Loans

Disclaimer

Credit Card:

Credit Score:

Personal Loan:

Home Loan:

Fixed Deposit:

Copyright © 2026 BankBazaar.com.